The Federal Reserve’s independence is under threat. Or at least the level of independence the institution currently enjoys is coming under serious challenge. President Trump has been absolutely clear that he believes policy rates should be lower. In some regards, this is nothing new. Throughout his first term in office, the President continually took to social media to argue for rate cuts. His interventions were so frequent that economists even had the opportunity to conduct a study of their impact on market expectations of future rates.

This time around, though, the attacks have moved beyond rhetoric and political pressure. The attempt to remove Governor Lisa Cook is working its way through the courts, and there is talk of reform of how regional Fed Presidents are appointed.

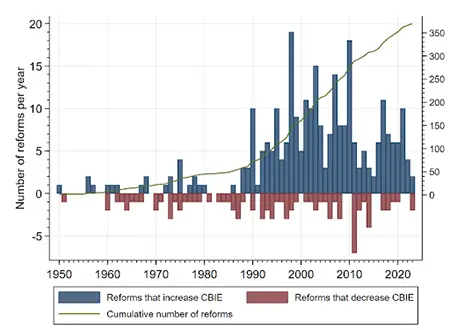

The broad history of central banks, across the globe, over the past few decades has been of rising levels of independence. Indeed, one recent study looked at measures of independence over 155 countries between 1923 and 2023:

I identify a total of 370 reforms to central bank design, which highlight a remarkable global shift towards enhancing the independence of monetary authorities. This shift is particularly notable in the context of recent global challenges that emerged following the 2008 global financial crisis, the COVID-19 pandemic and the recent resurgence of inflation experienced by many high-income countries since mid-2021, which have revived the debate on the role and scope of central banks. The findings in my paper contribute to these ongoing discussions, offering a nuanced understanding of how central bank independence has been shaped and reshaped over a century. The increase in the degree of central bank independence, observed across countries with varying levels of economic development, signals a broader recognition of the importance of independent monetary policy in maintaining economic stability.

A trend made clear by a striking chart:

Although one should note that the major steps towards more independence mostly occurred in the 1990s, and that the record since the 2008 crisis is somewhat more patchy.

Whether or not President Trump will get a more compliant Fed is hard to say. But this week, the Clark Center’s Finance Experts Panel was very clear on the potential implications.

Asked whether ‘a substantial loss of Federal Reserve independence would substantially increase the overall nominal cost of U.S. government borrowing’?, some 94% of respondents – weighted by confidence – either strongly agreed or agreed.

Asked whether ‘a substantial loss of Federal Reserve independence would substantially raise risk premia on long-term U.S. government debt’? – and again weighted by confidence – 90% of respondents either strongly agreed or agreed.

Those headline answers are fairly clean-cut. But there was a higher degree of nuance in the comments the experts offered up. Much, as ever, depended on competing definitions of ‘substantial’.

As Campbell R. Harvey of Duke Fuqua put it ‘I agree it would increase the cost of borrowing but it is not obvious it would “substantially” increase the cost of borrowing. Currently, there is no credible competitor to the dollar as reserve currency – even with a less independent central bank’.

A few different mechanisms were raised as to how a loss of independence would lead through to increased borrowing costs and risk premia. Douglas Diamond of Chicago Booth noted the role of inflation expectations, ‘Governments without independent central banks and with large nominal debts have taken monetary policies that increase inflation. The market will anticipate this and price in more inflation’. Whereas Stijn Van Niewerburgh of Colombia Business School also noted the role of uncertainty in elevating risk premia, ‘there would be substantial policy uncertainty that would raise the risk premium on long-term debt’.

The Clark Center’s own Anil Kashyap commented that, ‘the timing of when it happens will be hard to tell, but the list of countries where this is happened shows that the direction of travel is certain’ and pointed to a recent op-ed he co-wrote in the Wall Street Journal.

As that piece concluded:

Credibility in economic policymaking is built slowly, through practice and respect for processes, and can be lost quickly if those processes are disregarded. Preserving credibility is essential because it benefits all Americans by keeping the costs of borrowing money lower, supporting sustainable growth, and maintaining global confidence in U.S. institutions. Once lost, it is costly and time-consuming to rebuild. Protecting it must remain the central priority of U.S. economic policy.

That point on credibility is key. Credibility is, to an extent, a question of perception and expectations, and, in both cases, the direction of travel matters.

Take for example, the Bank of England. On many measures, it is fundamentally much less independent of the British government than the Federal Reserve is of the wider US executive branch. The government has far more control over the appointment of members of the Monetary Policy Committee and has the power to change the Bank’s inflation target whenever it desires (even if this power would only ever be used cautiously). According to Romelli’s rankings, the BoE scores just 0.44 on his central bank independence ranking (out of a potential 1.0) compared to the Federal Reserve’s 0.61. And both banks are well below the transnational European Central Bank’s score of 0.9.

The Bank of England is generally regarded as a credible and independent central bank, and yet it is less ‘independent’ than the Fed. This does not mean that the steps that reduced the Fed’s independence to the level of the Bank would be consequence-free. When it comes to central bank independence, the direction of travel may matter just as much as the final destination.