This week the Federal Reserve held its key policy rate steady at 4.25%-4.5% and the so-called ‘dot plot’ (the best guess forward projections of Federal Open Market Committee members) continued to show two cuts were expected this calendar year. One might assume, given the lack of change in either the policy rate or the immediate forward guidance on the likely path of rates, that monetary policy has achieved one its key aims; that of becoming boring and predictable. In reality though, and through no fault of the Fed itself, monetary policy has rarely been so interesting or the decisions of the FOMC so hard to call.

Monetary policymakers, much like everyone else trying to make sense of the economy, have been left waiting to see exactly where US trade policy will be on July 8th when the 90-day pause on the Liberation Day tariffs comes to an end. So far the promised flood of trade deals has been more like a trickle and the White House’s intentions are, as ever since January, tricky to read.

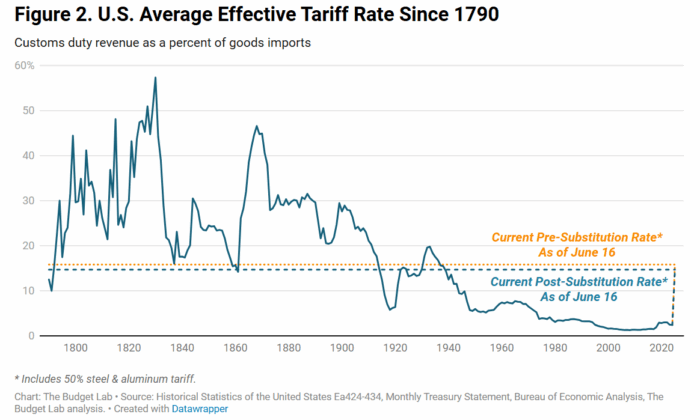

According to the Budget Lab at Yale – which now finds itself forced to calculate the average tariff rate twice each month, so frequent have been the changes – the effective tariff on US consumers now stands at, after likely substitution effects, now stands at 12.3%. This is, as their chart makes clear, a historically high level compared to recent decades:

And of course, there is every chance that this already decades-high effective tariff level could head much higher if many of the paused ‘reciprocal’ rates are reapplied in July.

But if it is clear that taxes on imports are the highest they have been in many years, what remains more opaque is the exact breakdown of who will bear the ultimate costs of this.

As Chairman Powell put it this week whilst answering reporters’ questions:

“Everyone that I know is forecasting a meaningful increase in inflation in coming months from tariffs, because someone has to pay for the tariffs … between the manufacturer, the exporter, the importer, the retailer… People will be trying not to be the ones who can pick up the cost. Ultimately, the cost of the tariff has to be paid, and some of it will fall on the end consumer.”

In other words, whilst it is unclear exactly how the costs of the new tariffs will be shared out it is likely that a substantial proportion will fall onto consumers and push up retail prices. Inflation will increase but it is unclear by exactly how much.

If the Damoclean sword of the Liberation Day tariffs were not still hanging over the American economy it seems likely that the Fed would already be cutting interest rates.

For several months now the soft data, based on surveys and confidence, has been signalling real economic weakness is coming down the line even if the hard data has been a bit more robust. But in recent weeks the hard data too has taken a turn for the worse.

Retail sales took their monthly biggest tumble in two years in May, although much of that likely reflects the unwinding of purchases being brought forward earlier in the year in order to front run tariffs.

The weekly initial jobless claims figures also point to a softening labour market with the four week monthly average figure, which smooths out some of the volatility of an often volatile series, at its highest level since August 2023. Housing data too is beginning to signal the economy is entering a weaker phase with permits for new builds of single family homes also falling to their lowest level since 2023.

Given that inflation has, in recent prints, come in at a more benign pace than widely expected one might have expected the Fed to react to mounting evidence of a slowing economy by cutting rates. Certainly, that seems to be the view of President Trump who has once more taken to castigating Chairman Powell for holding interest rates constant.

But until there is clarity on tariff rates it is hard to make a judgement call on the required level of interest rates. It was notable that the dot plot from the Fed this week showed an unusually high level of dispersion. Seven of the nineteen policymakers believed no cuts would be made to the policy rate this year. As Powell put it at the press conference it is an ‘unusually foggy time’ for anyone trying to forecast near term developments.

The Fed would rather see a few more months of data – and, perhaps even more crucially, see where tariff policy is by the end of July – before playing its hand. As Powell said this week, “no one holds these … rate paths with a great deal of conviction, and everyone would agree that they’re all going to be data-dependent”.

The Fed, like just about everyone else watching the US economy, needs to see what happens when the 90 day pause in reciprocal tariffs comes to an end before deciding on its next steps. Fed watchers are increasingly becoming White House watchers.