By any reasonable definition, New Zealand is a small economy. The latest estimates from the International Monetary Fund suggest that the Pacific Nation’s GDP, weighted by purchasing power parity, represents just 0.2% of total global output. But the Reserve Bank of New Zealand (RBNZ) has been something of a trailblazer when it comes to monetary policy strategy, and an example that has been followed globally.

Back in 1990, the RBNZ was the first central bank to adopt an inflation targeting regime. As a useful paper from the London School of Economics makes clear, the process of adopting an inflation target began in monetary failure. In the mid to late 1980s, New Zealand suffered from high and volatile inflation, and the country’s government made bringing the rate of price changes back under control a priority.

The framework that evolved over the next four years was the culmination of various strands of economic thought and the principles that were underpinning the wider reform of New Zealand’s public sector at the time. The framework that emerged was essentially the Barro-Gordon solution to the issue of inflation bias. This involved hiring an inflation-averse central banker—one given operational independence and a mandate to drive inflation down to a manageable level in a transparent manner. The Reserve Bank Act (1989) used four related ideas to support price stability. These ideas were: providing the Reserve Bank with operational independence; pursuing a single objective of price stability; giving the Governor authority to act as a single decision maker, and; ensuring the Reserve Bank provided transparency in its approach. This was the birth of inflation targeting—the start of a new era for monetary policy.

Granting the central bank operational independence and giving it the job of maintaining price stability was pretty much exactly what the academic consensus suggested by the late 1980s. But the notion of having an explicit inflation target to aim at was new.

The RBNZ’s innovation was to make the new target for inflation explicit and to be, by the standards of the time, extremely transparent about how it operated.

Underpinning all of these measures was transparency. To ensure that the Reserve Bank used operational independence appropriately, it would have to deliver a high degree of transparency in how it formulated policy. The Act required the Bank to publish regular statements on monetary policy decisions and for these to be laid before Parliament. These documents would later evolve into important quarterly updates of the economic outlook. The inflation targeting range itself—0 to 2 percent—was very transparent for the times, anchoring expectations in the process. This could have damaged credibility if the target were not met. This was considered to be one of the many risks associated with the pioneering of inflation targeting.

The explicit target helped to abhor inflation expectations amongst the public and firms and came to be seen as credible. In effect, having an explicit target turned out to make hitting it easier.

Over the following two decades, many central bankers – including those in the emerging economies – adopted the same techniques.

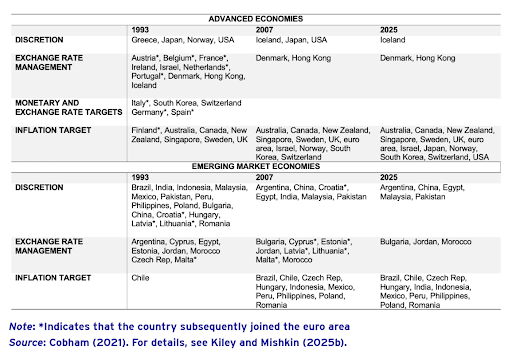

As a forthcoming chapter from Mishkin and Kiley sets out (recently summarised at VoxEU), an independent central bank, working towards an explicit inflation target, is now a very common organisation for monetary policymaking institutions. Some central banks still operate under the discretion of their heads (or in some cases governments), but this is far less common than it was in the early 1990s, and few nowadays set interest rates in relation to an exchange rate target.

The Fed was a relatively late adopter of modern inflation targeting. Whilst it operated to an implicit inflation target, this was not openly communicated to the public until 2012. As a helpful paper from the Richmond Fed explains, Chairman Greenspan was worried in the 1990s that making the target public would constrain what he saw as the needed discretion of policymakers.

The January 2012 statement on Longer Run Goals and Monetary Policy Strategy made the decade-and-a-half-old implicit 2% target an explicit one.

The updated version of that long run strategy statement was released in August 2020, and whilst that may have been during the global pandemic, it was more reflective of what were seen as the pressing monetary policy problems of the 2010s – notably a long period of low inflation and near-zero rates.

As the Richmond Fed explains:

In August 2020, the FOMC released an updated Statement on Longer-Run Goals and Monetary Policy Strategy that maintained the 2 percent target. It made several changes, however. Most notably, it acknowledged that inflation since 2012 had frequently been below 2 percent, and so it stated that after such periods, the committee would allow inflation to rise “moderately above 2 percent for some time,” bringing the long-term average back to target. It also changed its approach to employment: Where the 2012 statement indicated that the committee would move to reduce employment if it thought it had surpassed what it viewed as “maximum” employment, the new statement indicated that it would only want to reduce employment if it was necessary to keep inflation under control. Finally, it expressed concern that with interest rates near zero at the time, future policy might be constrained by the zero lower bound, increasing downward risks to employment and inflation.

At the time, this divided expert opinion. The Clark Center’s US Experts Panel was asked in September 2020 whether ‘the Fed’s revised strategy to focus on employment shortfalls and a more flexible interpretation of the inflation target will make little practical difference to monetary policy outcomes over the next decade’? Weighted by confidence, 33% of respondents agreed, 37% were uncertain, and 31% disagreed. That represents one of the least consensual results in the long history of the expert polls.

Almost five years on, though, the views of the experts have shifted somewhat.

Asked this week whether ‘The Fed’s revised strategy announced in 2020 – focusing on employment shortfalls and with a more flexible interpretation of the inflation target – has made little practical difference to monetary policy outcomes in the past five years’, just 14% of respondents (again weighted by confidence) agreed, 37% were uncertain and 48% disagreed.

In other words, whilst uncertainty remains high, the consensus has definitely moved in the direction of believing that the 2020 strategy has made a practical difference to policy. Whether those practical differences were for the better or the worse will be the subject of a future column.