A couple of months ago, your columnist noted that the US economy was living in the pause; the 90-day period during which the Liberation Day tariffs had been suspended, but during which it was unclear exactly what would come afterwards. It seemed unlikely that the Federal Reserve would move policy until greater clarity on trade policy emerged.

The pause, though, is now over. Over the last few weeks of July and into early August, the new tariff rates for major – and minor – US trade partners were announced. The European Union, for example – after some back and forth – has been left facing a 15% import tax on most exports to the United States following a late ‘deal’ struck at a golf resort, owned by President Trump, following a late-notice summit in Scotland. Switzerland, though, has somehow ended up facing a tariff of 39% on 18.6% of its exports, which head to the United States, a rate even higher than that threatened by the original package announced in the White House Rose Garden this Spring.

Even though the 90-day pause is over, trade policy uncertainty remains elevated. Few foresaw, for example, the sudden doubling of tariffs on India – from 25% to 50% – supposedly due to that country’s importing of Russian oil.

But whilst the final shape of the new administration’s tariff policy is not yet in place, the broad outlines are at least clear. The big picture is that tariffs are at multi-decade highs.

The Yale Budget Lab reckons that:

Consumers face an overall average effective tariff rate of 18.6%, the highest since 1933. After consumption shifts, the average tariff rate will be 17.7%, the highest since 1934.

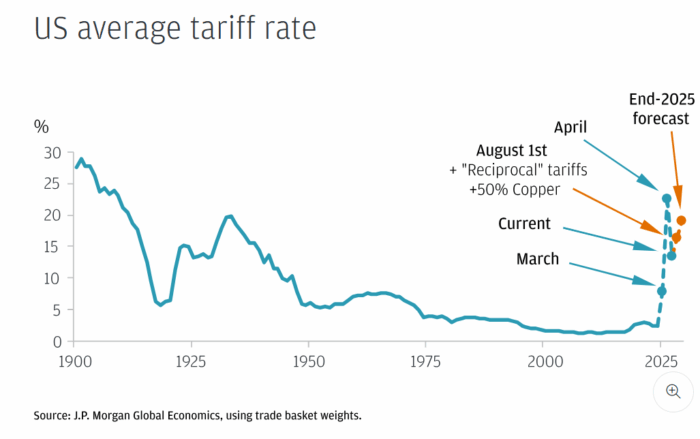

JP Morgan helpfully put their own calculations into graphic form this week.

Overall tariff rates may not be quite as high as those announced in early April, but they are, nonetheless, still the highest for almost a century and much higher than almost any Wall Street analyst was forecasting back in January.

It is instructive to look back to where markets were at the time the pause was unveiled in April. The original imposition of those tariff rates triggered a vicious market reaction with US equities, US bonds, and the dollar selling off at the same time – a most unusual event. Indeed, whatever the administration might claim, it is hard to avoid the interpretation that the original 90 pause was entirely a response to that sell-off.

Things look rather different now. The S&P 500 has rallied by around 30% since April 8th, with that rally led by tech and AI-exposed firms. The yield on ten-year US government Treasurys has fallen from around 4.5% to 4.25% as prices rose. Only the dollar has continued to lag with the broad dollar index down a couple of percentage points since the early April lows.

This is a fairly remarkable set of returns. If one had told most equity strategists and asset managers in mid-April that, once the 90-day pause was over, US tariff rates would be the highest since the early 1930s and closer to the Liberation Day rates than those before, then very few would have guessed that US equities would be almost one-third higher by mid-August.

The tariffs on the EU are a case in point. A 15% tariff on imports from the European Union is a very big deal. Under any other President in recent history, such a tariff rate would have come as a huge shock. Even back in January, after President Trump’s election but before his inauguration, 15% was at the very top end of analyst expectations – most expected some sectoral tariffs and more bluster than action. And yet compared to threatened rates of 25% or 30%, ‘just’ 15% can seem to come as almost a relief. Trade policy has become the art of boiling a frog slowly.

But while a tariff of 15% on the EU is indeed lower than a tariff of 30% and whilst an overall average tariff rate of around 18% is lower than an overall tariff rate closer to 25%, they still represent a large shock to US consumers and firms and one that has not yet been entirely felt.

In reality, the shock is even larger than analysts expected late last year. The consensus view was that President Trump’s policy mix would see the dollar gaining in value and offsetting the impact of tariffs. Instead, the dollar was weakened, magnifying the costs.

Either US importing firms will try to swallow the cost and see their margins squeezed, or they will pass the price rises onto consumers, pushing the price level upwards, or, most likely, some combination of the two. None of these scenarios are bullish, in the medium term, for equities.

The pause may be over, but the pain is just beginning.