Prediction markets, exchanges where market participants can trade contracts based on unknown future events such as sports results or the outcomes of elections, are booming.

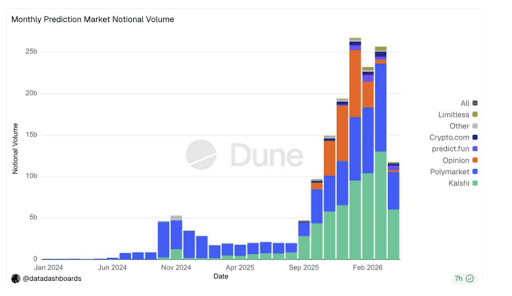

One recent report looked at trading volumes over the past few years and came complete with a rather striking chart.

(The final data point on this chart represents partially month to data incomplete data, rather than a fall in monthly volumes)

By any definition, this is explosive growth. And it may have further to run:

Industry projections cited in the report suggest prediction market volumes could reach $240 billion annually this year, with longer-term forecasts pointing toward the trillion-dollar mark.

That trajectory no longer seems far-fetched. Prediction markets have seen significant momentum since the 2024 US presidential election, benefiting early movers such as Polymarket and Kalshi. Both platforms are reportedly raising substantial capital at valuations exceeding $20 billion.

While the vast majority of trading activity relates to sports, media attention has tended to focus on political and geopolitical markets. The move in prediction markets to forecast a victory for President Trump in the summer of 2024 received a great deal of attention from financial market participants and may have helped kickstart the so-called Trump Trade of going long the dollar, US equities, and crypto, which dominated markets until that November.

This January, a sudden, sharp move in the markets based on the odds of a US military intervention in Venezuela – just hours before such an intervention occurred – raised a few eyebrows and has now led to criminal charges.

The US special forces soldier who made thousands of dollars betting on the removal of Venezuelan President Nicolás Maduro has pleaded not guilty to charges that he used classified information to profit.

Gannon Ken Van Dyke, 38, was arraigned in New York federal court on Tuesday after being accused last week of betting on Maduro’s January capture before the information was publicly available.

The US government contends that he allegedly made trades on Polymarket, a crypto-powered platform, on the basis of classified information, winning more than $400,000

But while such markets may be open to abuse from insiders with non-public information, they also potentially offer a great deal of useful information – including potentially for economic policymakers.

Our results highlight several key advantages. First, Kalshi’s forecasts for the federal funds rate and CPI provide statistically significant improvements over fed funds futures and professional forecasters, all while providing continuously updated full distributions rather than infrequent point estimates. The mode of the Kalshi distribution, for example, has perfectly matched the realized federal funds rate by the day of each meeting since 2022, a feat not achieved by either surveys or futures. Second, these markets capture rich distributional dynamics—such as tail risks and asymmetries in higher moments—that are unavailable from traditional sources. For instance, we find that monetary policy press conference shocks tend to significantly reduce skewness in the Federal Funds rate distribution. Third, the accessibility of Kalshi to retail traders introduces a perspective distinct from institutionally dominated markets, potentially offering a complementary lens on expectations formation.

Together, these findings suggest that prediction markets can serve as a valuable complement to existing forecast tools in both research and policy settings.

Of course, most money traded on prediction markets is betting on sports rather than economic statistics. And that has led to worries from some regulators that what is essentially a form of gambling is not being regulated as such. As a useful summary in the Stanford Law Review, from a former SEC Commissioner, noted last month:

How are prediction markets different from online gambling, and why does the distinction matter?

The answer depends entirely on whom you ask. Kalshi and Polymarket, the primary online event markets, claim their markets are fundamentally different from traditional gambling because there is no “house” that sets the odds and acts as the counterparty to all positions. Instead, prediction markets are structured more like traditional futures markets in which no wager exists unless a person on one side of the market is willing to do business with a person on the other side. The market sets the odds in the Kalshi and Polymarket models, not the casino, or “the House.” The states respond that this is a distinction without a difference because the end result is functionally indistinguishable from a traditional sports betting market.

On the first issue, the panel was asked whether such markets provide substantially more accurate forecasts than traditional methods, such as surveys of professional forecasters. A plurality of 37% of respondents, weighted by confidence, expressed uncertainty, with 5% strongly agreeing and another 31% agreeing. 17% disagreed, and 9% strongly disagreed. This was hardly a decisive result, but it did suggest that the panel leaned towards finding some value in such markets. It may be that over time, as more data and studies become available, confidence levels in prediction market-derived forecasts arrive.

On the second issue, the results were more decisive. Asked whether retail participants would be better off if such markets were regulated more like gambling than financial derivatives, 19% of respondents (again weighted by confidence) strongly agreed, and 38% agreed.

The panel then might see some value in the forecasts derived from prediction markets, but would still prefer if they were regulated more like gambling markets.