Over the last few years global equity market investors, and especially those closely following US markets, have devoted an awful lot of time to thinking about the future of artificial intelligence (AI). The promise of speculator returns, and the potential of large first moved advantages, have seen the price of AI-exposed firms – and in particular those providing the chips, other hardware and raw compute power required for the latest models – soar. There has been a huge boom in capital spending from the so-called ‘hyperscalers’.

As is ever the case with rising markets, there have been all the usual warnings about a potential bubble. While few analysts really doubt that the breakthroughs in AI in recent years represent real technological progress, plenty have expressed worry that the valuations attached to AI-leaders are becoming tricky to justify. The oft-cited example has been the dot-com boom and bust of the late 1990s and early 2000s: the internet has, in many ways, exceeded even the more optimistic projections made two to three decades in terms of reach and usage – and yet many of the stock darlings of that period either fell by the way side .

Recent weeks though have seen markets reacting to a new worry. Rather than fretting about AI underdelivering on its promises, some investors seem to be spooked by the idea that it could over deliver.

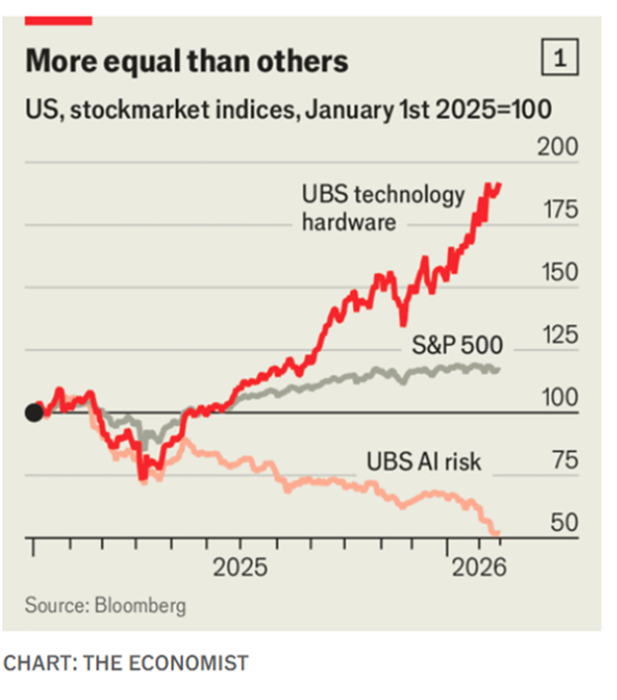

For all the recent geopolitical drama, the S&P 500 share index of big American firms sits almost exactly where it did at the end of 2025: just shy of a record high. Beneath the surface, however, the churn in America’s financial markets has been furious. A panic about what artificial intelligence will do to business models has prompted software firms’ stock prices to tumble: they are a third below a recent peak last year. On February 23rd IBM’s slumped by 13%, owing to vague worries about what AI means for the tech veteran.

Their chart was a rather striking illustration of the sharp divergence in sectors.

The new fear, partially prompted by recent developments in tools such as Claude Code, is that AI will fundamentally undermine the business model of many existing firms in areas such as software, accounting, legal services and whole host of other white collar roles.

Of course, the rise of AI has always been accompanied by fears that the new technology could – in theory – cause productivity to surge and employment in the impacted sectors to fall. But, until recently, most assumed that surging productivity, potentially falling employment costs and rising profits would be good for the valuations of firms in these sectors.

One catalyst for the recent sell-off was a widely cited substack post from Citrini Reseach which set out what they were careful to call ‘a scenario’ rather than ‘a forecast’ for how AI could essentially eat the business model of many long-standing companies.

The euphoria was palpable. By October 2026, the S&P 500 flirted with 8000, the Nasdaq broke above 30k. The initial wave of layoffs due to human obsolescence began in early 2026, and they did exactly what layoffs are supposed to. Margins expanded, earnings beat, stocks rallied. Record-setting corporate profits were funneled right back into AI compute.

The headline numbers were still great. Nominal GDP repeatedly printed mid-to-high single-digit annualized growth. Productivity was booming. Real output per hour rose at rates not seen since the 1950s, driven by AI agents that don’t sleep, take sick days or require health insurance.

The owners of compute saw their wealth explode as labor costs vanished. Meanwhile, real wage growth collapsed. Despite the administration’s repeated boasts of record productivity, white-collar workers lost jobs to machines and were forced into lower-paying roles.

When cracks began appearing in the consumer economy, economic pundits popularized the phrase “Ghost GDP“: output that shows up in the national accounts but never circulates through the real economy.

Some might be tempted to call this ‘speculative fiction’ rather than ‘a scenario’. Either way it is an oddly gripping read compared to much investment research. But is it worth taking very seriously?

It is fair to say they were unconvinced. As might be expected, a large proportion of the experts were uncertain. Even taking a productivity boom as given, as the question did, much would depend on how the firms themselves reacted before even considering how stock markets would adjust their valuations. Weighted by confidence, 61% of respondents expressed uncertainty. Of the remainder 10% agreed, 21% disagreed and 8% strongly disagreed. While the majority of respondents emphasised uncertainty, those results point to some scepticism.

As the Center’s own Anil Kashyap put it, “There are just too many scenarios to quantify this. The Citrini Scenario assumes large organizations respond way, way more quickly than is plausible. If you work in a large organization, ask yourself whether your firm could pivot that quickly”.

Whether or not AI will fundamentally compromise the business models and reduce their equity valuations is a tricky call to make. But either way, a market that can be rocked by a substack post (even such a gripping one) is clearly a market that is nervous about something.