Around 24 million Americans buy healthcare insurance through the marketplace established under the Affordable Care Act (ACA), and, until the 31st December last year, the majority of those purchasers received a subsidy via a tax credit. But now those subsidies have been allowed to lapse.

As the Wall Street Journal reported this week:

Millions of Americans are starting to see their monthly health-insurance bills rise, a new pressure point for a nation still frustrated with the high cost of living.

Many of those facing the most substantial dollar increases are middle-income Americans who buy health insurance through the marketplaces set up by the government’s Affordable Care Act, known as Obamacare.

Moreno is one of the lead GOP negotiators involved in months of talks about a potential two-year revival of the enhanced Obamacare tax credits that lapsed Jan. 1. The senators involved have discussed immediate new restrictions such as an income limit, as well as more sweeping changes kicking in the second year, including expanding the use of health savings accounts.

But hopes are not riding very high on the prospect of a deal.

The Economist explained the background last month.

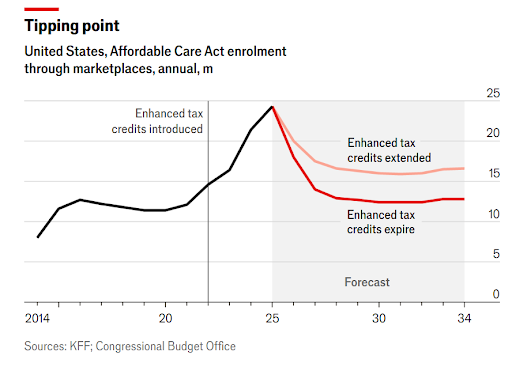

The expiring tax credits date from changes made to the ACA exchanges during the pandemic. Subsidies became more generous, eligibility was widened and households’ payments were capped. No one enrolling in health insurance through one of the ACA’s marketplaces has to spend more than 8.5% of their income on premiums. More than 40% of those enrolled now pay $10 or less a month.

And provided a helpful chart:

If Congress allows the subsidies to expire, monthly healthcare premiums will double, on average, for the more than 20mn Americans who rely on them. According to KFF, a non-profit health policy research group, the average annual premium payment will rise from $888 to $1,904. But costs will climb even more for millions of Americans. For example, premiums for a 60-year-old making roughly $60,000 annually in either Wyoming or West Virginia are set to jump by more than 400 per cent, according to KFF.

This week, the Clark Center’s US Economic Experts Panel weighed in on the economics of ACA subsidies. The results showed a large degree of consensus.

To begin with, the panel was asked whether “Without extension of the expanded public subsidies for Affordable Care Act healthcare plans, there would be a substantial rise in the number of Americans without health insurance”?

The answers were almost unanimous. Weighted by confidence, 95% of respondents either strongly agreed or agreed, with 5% expressing uncertainty. Although, as Julie Chevalier of Yale noted – pointing to a recent NBER working paper – the interaction with varying state-level policies complicates the picture.

Next, the panel was asked whether “Losses in the health and well-being of Americans who could no longer afford health insurance in the absence of the subsidies would exceed the savings from the expiration”? Here, the consensus was less decisive, but still very strong.

Again, weighted by confidence, 25% of respondents strongly agreed, 42% agreed, 27% were uncertain, and just 6% disagreed. As Larry Samuelson of Yale argued, “it is difficult to be precise about this trade-off, but experience shows that health insurance is cost effective in improving well being and shifting medical care away from emergency services to most cost-effective measures”. Hilary Hoynes of Berkley acknowledged that the evidence here is incomplete but pointed to a useful paper from 2020.

Finally, the panel was asked whether “The possible need for subsidies substantially in excess of those initially provided by the ACA indicates that other changes in the healthcare system are needed to enable broad-based access”?

The results were something of an indictment of the American healthcare market and system. While the panel no doubt disagrees on the specific reforms required, more than 90% of respondents, as ever weighted by confidence, either agreed or agreed strongly. The remainder were uncertain.

Several panellists pointed out that the United States has a system whereby healthcare costs are high by global standards, but outcomes are, at best, middling by comparison with other advanced economies.

As Richard Thaler of Chicago Booth put it, “We pay high prices and get mediocre outcomes so we know the system is bad but those making the big bucks will fight to keep the status quo”. As with so many thorny policy issues, this suggests that the problem lies as much in questions of political economy as it does in raw economics.