The last month has seen much in the way of, often justified, gloomy introspection from European policymakers. Isabel Schnabel, a member of the European Central Bank’s policy-setting executive board made a useful speech on the 2nd of October rather tellingly entitled “Escaping Stagnation”.

The raw facts speak for themselves, since the pandemic, the European economy has been weak even whilst growth on the other side of the Atlantic has been healthy. Between the fourth quarter of 2019 and the second quarter of 2024, the US economy grew by 10.7% and that of Canada by 5.5%. By contrast, the Eurozone as whole grew by just 3.9% with France and Germany weaker still at 3.7% and just 0.2% respectively. Germany’s near total-stagnation almost makes the UK’s weak 2.9% look respectable by contrast.

There can be no doubt that the post-pandemic years have been tough for the European economy. Rising global trade tensions, a more fractured world economy, and the energy price shock that followed on from Russia’s invasion of Ukraine have all contributed to the downturn. But more worrying still than all the global and geopolitically driven shocks which have buffeted the European economy over the last four or five years is a longer running weakness. A sense that the continent has been slipping further behind the United States in economic terms.

Two charts in particular that accompanied the Schnabel speech are worth a closer look.

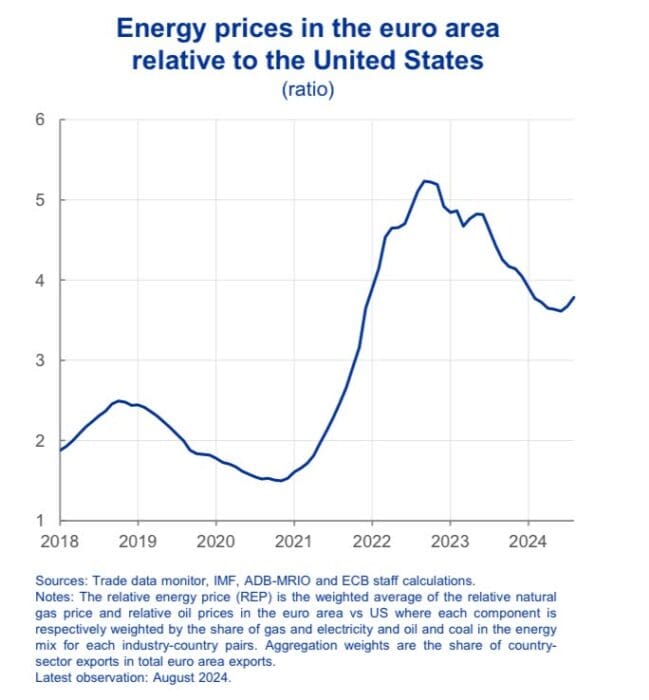

The first demonstrates the magnitude of the energy price shock which hit Europe between 2021 and 2023.

Perhaps, given this, one should not be surprised by the poor European growth figures since 2020. If anything, one might have expected an even weaker outturn.

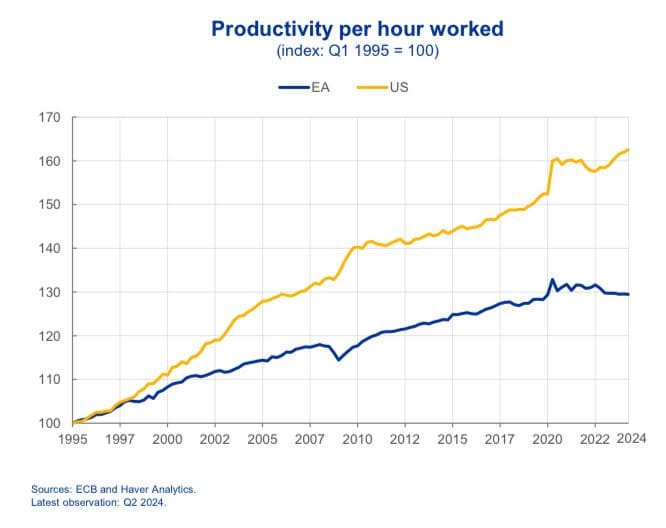

The much more worrying – and in the longer term probably the more significant – chart was far more straightforward. A simple look at American and European productivity back to the 1990s.

Since 1995 European output per hour worked, the ultimate driver of both economic growth and, more importantly, living standards has risen by about 30%. But US output per hour worked has grown about twice as quickly.

This was the gap that was the real concern of the other major bit of European elite-level introspective gloom over the last few weeks: the Draghi report.

At the bequest of the European Commission the former ECB head and Italian Prime Minister has prepared a long report on European economic weakness and the policies needed to overcome them. As the report notes:

The EU-US gap in the level of GDP at 2015 prices has gradually widened from slightly more than 15% in 2002 to 30% in 2023, while on a purchasing power parity (PPP) basis a gap of 12% has emerged. The gap has widened less on per capita basis as the US has seen faster population growth, but it is still significant: in PPP terms, it has risen from 31% in 2002 to 34% today. The main driver of these diverging developments has been productivity. Around 70% of the gap in per capita GDP with US at PPP is explained by lower productivity in the EU. Slower productivity growth has in turn been associated with slower income growth and weaker domestic demand in Europe: on a per capita basis, real disposable income has grown almost twice as much in the US as in the EU since 2000.

The report identifies several areas where Europe has work to do but one of the core areas of concern relates to the tech industry. As Mr Draghi writes:

the productivity gap between the EU and the US is largely explained by the tech sector. The EU is weak in the emerging technologies that will drive future growth. Only four of the world’s top 50 tech companies are European.

The panel weighed in on three related areas, beginning with competition policy. One near constant complaint from European tech firms – and those who invest in such firms – is that Europe’s more heavy-handed approach to what American’s typically call anti-trust policy has restrained the growth of the European sector. One reason, according to one tech major tech VC, that Europe has not produced a Meta or an Alphabet is that the authorities would have probably broken it up on competition grounds.

Asked whether “current enforcement of competition policy in Europe is not working to promote innovation and growth”, some 48% of respondents (as ever, weighted by confidence) either agreed or strongly agreed whilst 25% of respondents either disagreed or strongly disagreed.

That is best read as cautious support for the notion that over vigorous European competition policy has restrained innovation and growth. Of course, one might argue that was a price worth paying to prevent the abuse of monopoly positions.

The panel was then asked whether “European Union bureaucracy and regulations are a substantial constraint on innovation in Europe”. There was a resounding agreement in this case. 73% of those responding either agreed or strongly agreed with just 9% in disagreement.

Lastly, the panel was asked to consider whether “the conduct of the dominant US tech companies in European markets (including lobbying and acquisition of start-ups and competitors) is a substantial constraint on innovation in Europe”. Again there was broad agreement, with 48% agreeing and 15% disagreeing. This is exactly what one might expect – large incumbents often seek to protect their position.

Regulations and competition policy alone are unlikely to be the sole driver of Europe’s weak technology sector and lack of innovation. As several panelists noted, the lack of venture capital and differing approaches to entrepreneurialism no doubt play a large role.

But regulation is at least one area where policymakers can, if they so choose, move relatively quickly. If European policymakers are serious about closing the productivity gap with the United States it is one place where they could make a useful start.