It can be hard to keep up. China meanwhile was subjected to an additional 10% tariff back on February 4th and then, for good measure, a further 10% this week. Next week 25% tariffs on steel and aluminium are due to go into effect and, in early April the administration has pledged to unveil its so-called reciprocal tariffs. The exact nature of that package is subject to wide debate with talk of US tariffs being set not only to match the tariffs charged by trading partners but also to take account of non-tariff barriers and possibly also value added taxes. It is, at best unclear, how such a fiendishly complicated set of measures would work in practice.

And alongside the reciprocal tariffs, President Trump has separately floated the notion of a 25% tariff on the European Union.

All of which is a rather long way of stating that US tariff policy is fast moving and very hard to follow. The twists and turns make for good copy for journalists covering the global economy but are a nightmare for firms trying to manage day to day cross border business, manage inventory levels and plan for the future.

It does seem, at least in the case of North America, that the approach has been to impose blanket import taxes first and then make exceptions later. The dropping of, and then swift reinstatement, de minimis exemption on small parcels from China followed the same pattern.

That leaves firms and investors not only trying to work out which of the threatened tariffs will actually be imposed and when but also second-guessing which sectors will have the political clout to gain themselves some breathing space.

The tariff blizzard, despite being regularly talked up by President Trump and many of his surrogates, on the campaign trail appears to have taken many investors by surprise. The assumption of many seems to have been that whatever candidate Trump might have said, President Trump would be more restrained in office when it came to trade policy whilst also cutting taxes and regulation.

Over the last year the Clark Center’s US Expert Panel has pondered the threat of tariffs on multiple occasions. The results have always been the same: tariffs will impose costs on the American and global economies. In December more than 80% of the experts, weighted by confidence, reckoned that tariffs and trade wars would lead to measurably slower global growth in the coming five years.

It is though worth stepping back from the tariffs themselves – which will likely raise prices for American consumers in the short term and cause a loss of economic dynamism in the longer term – and asking if the very manner in which they are imposed is causing additional economic pain?

This seems more than plausible.

The Brexit case study is useful here. The consensus view amongst economists has long been that the United Kingdom’s withdrawal from the European Union’s single market and customs union means putting trade frictions into what was once an almost frictionless trading relationship. Trade friction leads to less trade and less trade and competition to slower productivity growth. The UK’s Office for Budget Responsibility estimates the long term hit to GDP levels, relative to a no-Brexit counterfactual, to be worth around 4% of GDP.

But, and this is the more interesting analogy, whilst Britain did not leave the European Union until January 2020, the economic hit from Brexit began straight after Britain voted to leave in June 2016. Some of that was markets and firms anticipating the likely impacts but much of it came through the uncertainty channel. The United Kingdom spent three and half years very publicly debating what its trading relationship with its largest trading partner should look like, with vastly differing versions mooted at various points. Many firms paused or cancelled planned investments as a result. And that weakness in business investment was a material drag on economic growth from 2016 until the pandemic.

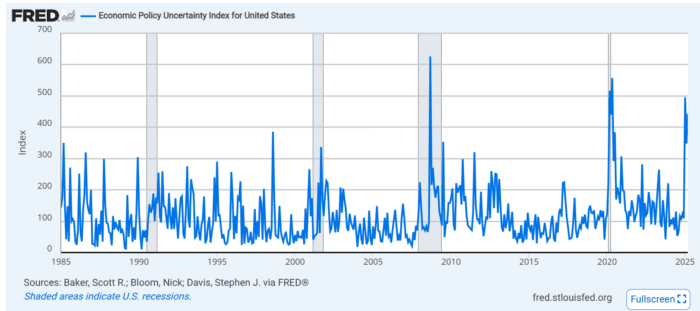

Could something similar now play out in the United States? A 2015 paper by Scott R. Baker, Nicholas Bloom and Steven J. Davis on measuring economic policy uncertainty suggests it could. The authors found that high levels of policy uncertainty (as measured by newspaper articles) is associated with higher stock market volatility and foreshadows reduced investment and employment levels.

It will likely rise further until the shape of tariff policy becomes clearer.

The economic damage wrought by the new tariffs then could well come not just from the end point but also from the path taken to reach it.