To European observers, one oddity of the American election was the seeming disconnect, to foreign eyes at least, between the tone of the economic policy debate and the official economic data. Whilst US consumers seemed oddly downbeat – and polling showed a large segment of the population pessimistic about economic performance since 2021 – to outsiders, US growth since the pandemic made it the envy of the world.

In the German case, there is no mysterious disconnect. Consumers are miserable and any economist looking at the numbers can straight away see why.

The facts are stark. The German government forecasts that GDP will contract this year, following on from a contraction in 2023. That would make for Germany’s first two-year recession in more than two decades.

Isabel Schnabel, a policy setter at the European Central Bank, summed up the situation well in a speech last month. It is striking just how much of the wider Eurozone economic weakness of recent years can be laid at Germany’s feet.

In fact, much of the euro area’s dismal growth performance since we started raising our key policy rates can be attributed to a small group of countries, including Germany, Finland and Estonia.

If one were to plot growth in the euro area excluding Germany, for example, activity in the currency area would have been remarkably resilient in the face of the sharpest monetary policy tightening in decades and a war raging at the EU’s doorstep. Only a few advanced economies, most notably the United States, have expanded at a faster pace during this period.

Of course, talking about the Eurozone economy excluding Germany is rather like talking about the American economy excluding California and Texas; interesting but not especially helpful for policy.

It is, on one level, hard to imagine a more difficult set of global economic and geopolitical shocks for Germany’s economy to navigate than those experienced between 2021-24.

The country is, by the standards of other advanced economies, usually reliant on manufacturing and export-focussed. What is more, the country was a heavy user of Russian energy.

The energy price spike and the loss of Russian export markets was a severe blow. But developments in China have been just as crucial.

Over the course of the 2000s and 2010s, the Sino-German economic relationship deepened considerably. The two exporters seemed to grow in complementary ways. Germany imported consumer goods and intermediate components from China whilst exporting cars, chemicals, and machine tools back in return. China, though, is now able to produce for itself much of what was previously imported from Germany.

In several key markets, China has transformed from a major German customer to a fierce competitor in the space of just a few short years. Cars are the obvious example. As recently as 2019, China exported fewer than a million cars a year whilst Germany managed closer to four million. This year China looks set to export more than six million automobiles and Germany under three million.

It might perhaps be comforting to blame Germany’s economic woes entirely on external developments. Sadly though, that is not the case.

As Ms. Schnabel noted in her October speech, Germany’s economy grew by just 1% in the five years to the end of 2021 compared to 5% in the rest of the Eurozone over the same period and more than 10% in the USA. The problems and weaknesses predate the shocks of more recent years.

As the IMF helpfully summarized in its Article IV report on the state of the German economy, this summer, the German economy faces structural headwinds.

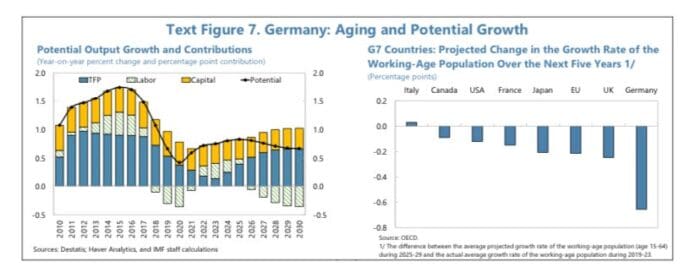

One of those, as illustrated by an IMF chart, is a demographic problem that will, on the central forecast, be a drag on growth in the future.

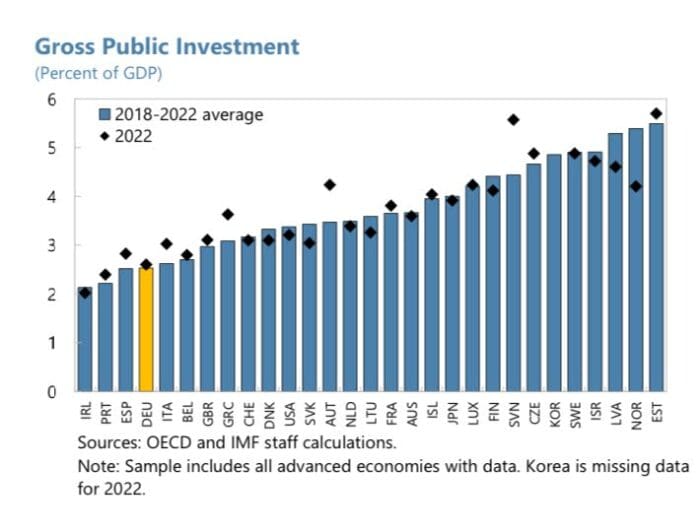

Alongside that though is an investment problem. Public investment levels look low in Germany, especially when compared to her peers.

Germany’s infrastructure – both physical and digital – appears increasingly creaky.

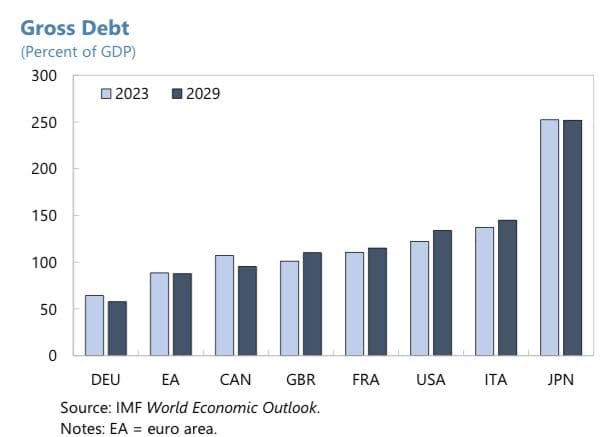

What makes this especially frustrating is that there is little doubt that Germany has more fiscal space to increase investment in the needed infrastructure than many other rich countries. Debt levels are much lower.

One major problem, holding back such spending, is the country’s so-called debt brake which imposes a constitutional cap on Federal Government borrowing.

In the 2000s and early 2010s, at a time of rapidly rising government borrowing across the eurozone as a whole, German fiscal prudence was welcomed by markets and the country’s debt served as a safe haven during the various eurozone crises. Now though, this debt brake appears to be doing more harm than good.

Reform of the brake will be a major theme in next year’s election. That should be welcome news to the Clark Center’s European Experts Panel. They looked at the debt brake earlier this year and whilst recognizing that such rules can be a helpful source of discipline, also feared that it was preventing much-needed public investment.