Perhaps the next time I am asked if I have any stock tips, I will simply refer the questioner to the Finance Experts Panel’s recent survey on stock picking. The answers might not be what those seeking equity investment ideas want to hear but they were at least extremely decisive.

The panel was asked to comment on two propositions and, extraordinarily, neither of them attracted any answers of uncertainty, disagreement, or strong disagreement. In both cases, the only debate was between whether respondents agreed or strongly agreed.

Firstly, the panel considered whether: “In general, absent any proprietary information, a retail equity investor cannot consistently make accurate predictions about whether the price of an individual stock will rise or fall on a given day”. Weighted by confidence, 78% strongly agreed and 22% merely agreed.

Secondly, the panel considered if, “In general, absent any proprietary information, a retail equity investor can expect to do better by holding a well-diversified, low-fee, passive index fund than by holding a few stocks”. This time 77% strongly agreed and 23% agreed.

In the view of the experts, the best stock tip is “don’t pick individual equities, instead hold a diversified, low-fee, passive index fund”.

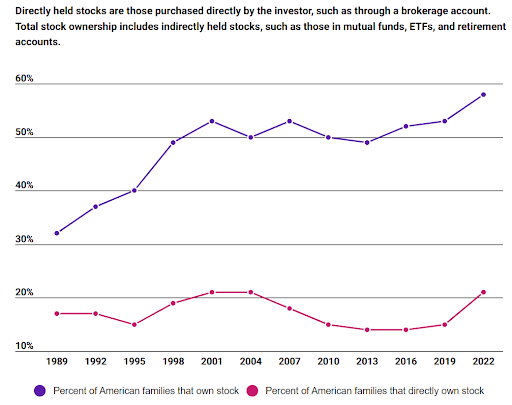

The good news is that slowly but surely, people do seem to be listening. As a recent article on the Motley Fool noted, almost 60% of Americans hold stock in some form or another but just one in five hold individual stocks directly.

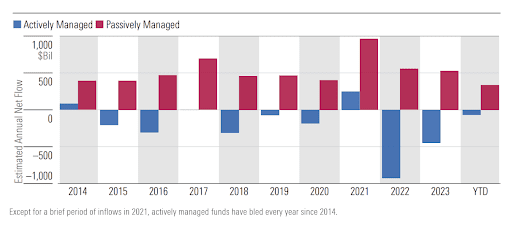

Of course, not all of those holding mutual funds, ETFs, or similar will be investing in passive strategies. But the share of assets under management managed passively has been rising in recent years. Morningstar, a financial news service, reckons that total passive assets under management surpassed active assets under management in 2024 for the first time in the United States. Their data shows a persistent outflow from active funds over most of the last decade and a larger inflow into passive funds.

Although they do note that the trend is less visible outside of America where passive strategies are better established.

The rise of the passive fund is one the clearest practical examples of the thinking coming from economics and finance academics being put to use in the real world. Ever since the 1960s there has been a firm consensus, in the academic community at least, that equity markets are – in the main – efficient. That is to say that new information is priced as it becomes available. Given this, it is hard to justify the high fees often levied by active managers. If one wants exposure to equity markets, then a passive fund – which simply aims to capture the returns of the market as a whole – is, as the panel notes, the most effective strategy.

In his response to the poll Anil Kashyap, the Clark Center’s Co-Director, pointed to Ken French’s Presidential Address to the American Finance Association in 2008. It makes for rather stark reading for anyone pondering investing in an active fund.

Looking at data from 1980 to 2006, French attempted to quantify the costs of active management in the USA. As he put it:

How much do investors spend trying to beat the market? To answer this question, I start by estimating the total amount society spends to invest. I measure four components: the fees and expenses investors pay for mutual funds, including open-end funds, closed-end funds, and exchange-traded funds; the investment management costs of institutional investors; the fees investors pay for hedge funds and funds of hedge funds; and the costs all investors pay to trade. I then compare these costs to what society would pay if all investors held a passive market portfolio. The difference is the cost of active investing.

The figure he ended up with was a large one.

I find investors spend 0.67% of the aggregate value of the market each year searching for superior returns. Society’s capitalized cost of price discovery is at least 10% of the current market cap. Under reasonable assumptions, the typical investor would increase his average annual return by 67 basis points over the 1980 to 2006 period if he switched to a passive market portfolio.

Of course, if the idea of “beating the market” is so tricky for well-resourced investors with teams of analysts, regular access to company management, and expensive private data sources it is even trickier for individual retail investors, As Andrew Lo of MIT Sloan put it, “The competition in this endeavor, just among the top 10 investment banks, is intense, not to mention the hedge-fund industry, so retail investors don’t have a chance.”

The advice of the economists and Finance Experts surveyed to anyone asking for stock tips is clear: don’t, invest in a low-cost tracker instead.

Perhaps stock-picking by individual retail investors should be thought of not just as an investment approach but also as a hobby. Researching companies and choosing stocks may even be an enjoyable pastime for some. But those partaking should keep Ken French’s numbers in mind. Stock Picking is an expensive pursuit but then so are many other hobbies from golf to fly fishing.