Market expectations moved rapidly in the run-up to the event. One week before, the market was pricing in roughly a 65% chance of a 25bp cut and 35% chance of a larger move. By the time of the meeting itself, partially in reaction to what traders read as well-sourced pieces in the Wall Street Journal and Financial Times, that pricing had reversed.

The meeting was noteworthy in other ways too. Michelle Bowman, who preferred a 25 basis point move, became the first Federal Reserve Governor to dissent on a policy call since 2005 – almost twenty years ago.

In reality, the difference between a 25 and 50 point move at the September meeting is not as large as sometimes portrayed. What matters much more than the first step is both the eventual end point of the journey and the pace at which it will be made. In this context, a 50 point move might be taken as a signal that the Fed intends to move quickly in reducing rates or it could just as well be a sign that, with the benefit of hindsight, policymakers believe they should have started cutting earlier and are now playing catch-up. Or both of those interpretations could just as well be incorrect. It is this sort of guessing that makes following monetary policy fun (for a given definition of “fun”).

An easing cycle has clearly begun but no one is quite sure exactly where it will end. There is broad agreement between economists, Fed watchers, and traders that US growth has slowed and rising confidence that the recession scare that rattled markets earlier this summer was just that; a scare. Inflation has fallen, although it remains above target. The recent FT-Booth US Macroeconomists survey is a useful guide to the outlook.

What really complicates analysis though, and makes the outlook on policy especially unclear, is that those trying to work out exactly where rates are headed are, in effect, actually trying to answer two distinct questions.

The first is the familiar one: what is the outlook for growth and inflation? But just as importantly, traders and economists are also grappling with the issue of what level of rates are ‘neutral’ and whether this has changed in recent years.

The neutral rate – the level of interest rates at which policy is neither expansionary nor contractionary – is a tricky concept to pin down. Much academic – and policy-related – economic work over the last decade or so has focused on trying to measure (or more accurately, estimate) the level of so-called r*. With r* being the real rate of interest at which the economy would operate at full potential without generating additional inflationary pressure.

The broad consensus is that in the decade before the pandemic the level of r* fell driven by, depending on the analyst, a combination of demographic change, higher debt levels, rising inequality, and the process of globalization. Fed Governor Waller’s speech in Reykjavik earlier this year and a speech by then Bank of England Monetary Policy member Gertjan Vlieghe in 2016 both provide a useful policy-oriented discussion of the concept.

Since the pandemic though – and especially given the large upswing in inflation experienced in 2021-23 – the equally broad consensus is that r* has risen. But whilst most observers can agree that the neutral level of rates fell in the decades before 2020 and has risen over the past 36 or so months, there is little agreement on the magnitude of either shift. Goldman Sachs economics team, for example, recently made the case that the r* has risen more sharply in recent years than many policy-makers seem to grasp.

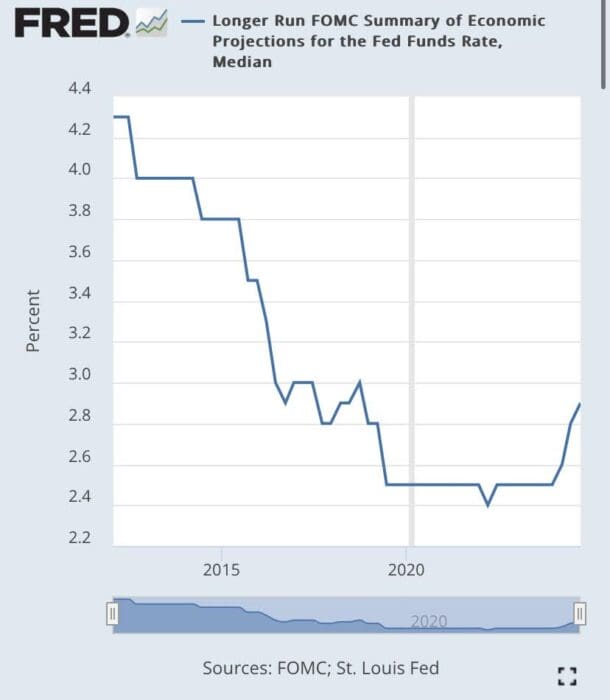

One useful way to follow the ongoing debate is to simply look at what Fed policymakers believe will be the longer-run level of their policy rate as a clue as to what they believe the level of nominal neutral rates to be.

A decade ago Federal Open Market Committee members thought that rates would eventually settle at around 4% (on the median estimate) but by 2020 that had fallen to 2.5%. That could be taken to imply a 1.5 percentage point fall in the neutral rate. But in recent meetings that median estimate has begun to tick back up.

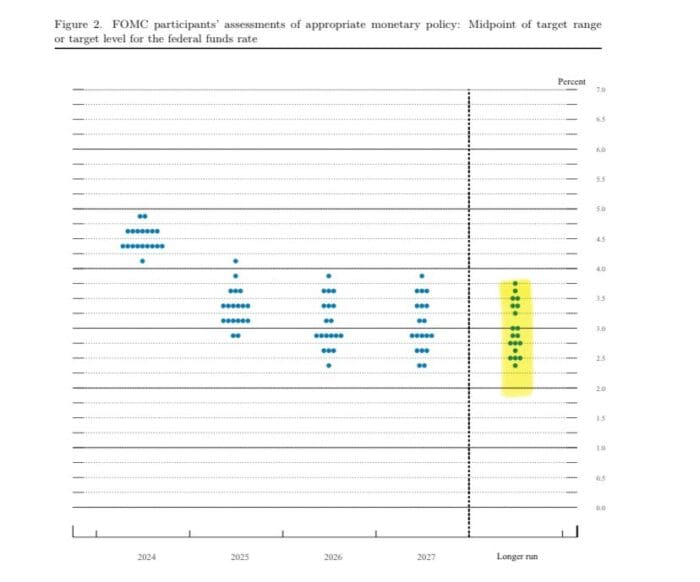

It is noteworthy though that even the FOMC’s own median view disguises a lot of nuance. The latest dot plot (highlight added by your columnist) makes clear the range of views on neutrality.

This divergence in views matters. The difference between, say, Fed Funds of 2.5% being neutral and Fed Funds of 3.5% being neutral is a large one. To state the obvious: one view implies that a Fed Fund rates of 3% would be contractionary and slow the economy and the other implies that the same Fed Fund rates would be expansionary and add to demand and inflationary pressure.

The easing cycle has begun but quite how far it will run remains exceptionally hard to call.