Sometimes it is helpful to step back and look at the, often slower moving, changes which may appear less dramatic on a week-by-week, or even month-by-month basis. A useful thought exercise is to ask oneself what economic and financial historians will reckon the major market trends of the 2010s and early 2020s to be when they look back from the vantage point of, say, the 2060s?

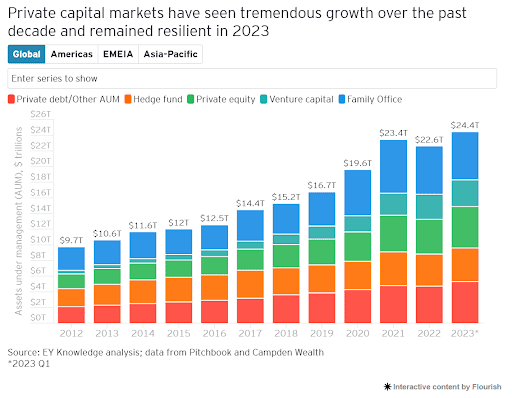

When it comes to the global economy, the economic historians of the future will have plenty to write about – the crisis of 2008-09, quantitative easing, the pandemic, and the global inflation of 2022-23 will all no doubt feature prominently. What thought of financial markets? There are some strong candidates for future interest; the unusually large outperformance of US equities over their rich world peers, the experience of a decade of ultra-low interest rates, and the increasing share of total market capitalization accounted for tech firms. But it may well be that, in a few decades time, the most interesting market development of the past 15 or so years will be seen to be a major change in the structure of markets themselves. The rise of private, as opposed to public, markets.

Private equity and private credit have both enjoyed long booms. On Global Markets has written on both in the last year.

As E&Y put it:

As private capital markets have become larger and more liquid, many successful companies have chosen to stay, or go, private. For many larger private companies, the option of staying private has also become more appealing. This is partly due to the reassurance of higher regulation standards in private company governance models. However, conditions in the public market have also played a part. These include increasing costs, and the daily, quarterly and annual public market disclosure requirements, which discourage companies from going and staying public.

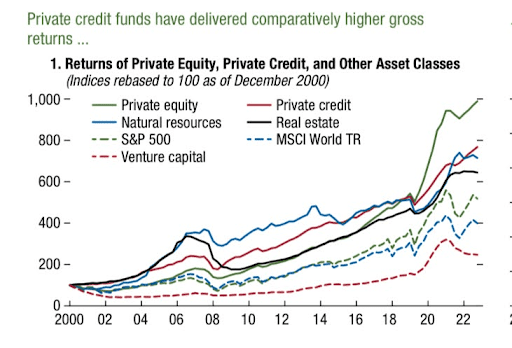

The 10-year picture also reveals that the performance of private markets has been consistently stronger and less volatile than that of public markets, especially since 2016.

Those higher returns were charted last year in the IMF’s annual Global Financial Stability Report.

The rise of both private credit and equity assets under management opens up important long-term questions about financial stability risks and the changing nature of corporate governance but also leaves regulators with a more immediate question: how available should such private markets be to retail investors?

Indeed, as On Global Markets has discussed previously, the private assets industry believes its future growth may well be dependent on retail money.

For the private equity sector, retail money seems to be the only way to maintain fast growth in assets under management. As Bain put it:

“…it is unclear whether the industry’s traditional sources of fund-raising (large institutions) can continue to support that kind of growth. Bain & Company projects that institutional capital allocated to alternative investments will grow 8% annually over the next decade.”

8% annual growth in assets under management is nothing to be sniffed at but falls short of the double-digit growth such firms have become used to and still target.

But should retail investors be prepared to hand over their savings? Before Christmas, the Clark Center’s Finance Experts Panel was asked if “a properly diversified 401k account should include private equity and private credit assets”.

The results showed a wide range of views. Weighted by confidence, 43% of respondents either strongly agreed or agreed, whilst 22% either disagreed or strongly disagreed. More than a third of respondents were uncertain.

John Cochrane of the Hoover Institute at Stanford, who was uncertain, made an important distinction in his comments: “Should be legal. Wise? The attraction is supposedly better returns, not diversification, low correlation. A lot of volatility and beta laundering. A bit closer to true market portfolio I guess. And good regulatory / tax competition against onerous treatment of public securities.”

Steve Kaplan of Chicago Booth, who was also uncertain, like many other respondents worried about the high level of fees generally charged by the industry in comparison to the lower charges available on passive trackers for public markets. “Strong evidence that private equity and credit provide diversification benefits over public securities at institutional level. Uncertainty in my answer is driven by question of whether 401K investors will get lower returns through higher fees and / or adverse selection”.

Other respondents noted the relative lack of vehicles for investment open to retail investors in comparison with the wide range of options in public markets.

Amongst those supporting the proposition, Andrew Lo of MIT Sloan argued that “Diversification can be improved with a wider set of assets”. Although, John Campbell of Harvard cautioned that “Private assets do have a role in a fully diversified portfolio, but discretion in marking values to market makes it easy to conceal risks which is dangerous for less sophisticated investors including typical 401(k) investors.”

At present the experts lean towards suggesting more retail participation in private markets although the level of uncertainty remains high. If the trends of the last decade and a half continue to play out, then it is a topic that more and more retail investors will have to grapple with.