Voters, for entirely understandable reasons, dislike both inflation and unemployment. They are not wrong to do so, both are things that economic policymakers generally try to avoid or at least minimize.

The problem is that, to a greater or lesser degree, the two macroeconomic failings tend to represent a trade-off. The tighter monetary policy usually associated with steps to reduce inflation works partially through slowing hiring and pushing up employment. Whilst tax cuts or additional government spending can increase the pace of economic expansion in the short run, driving down unemployment also risks pushing up the pace of price growth.

None of which is to say that the relationship between unemployment levels and the rate of inflation is ever exact, smooth, or stable. Policymakers cannot simply pick a certain combination of unemployment and inflation from a list of available options. Other factors – both domestic and external – affect both the rate of inflation and the level of employment at any one time, as well as their relationship to each other. But, managing the trade-off between unemployment and inflation is one of the challenges of macroeconomic policymaking.

For politicians, who unlike central bankers face elections, this trade-off takes policymaking away from the realm of macroeconomics and firmly into the domain of political economy.

By any conventional measures, the economic performance of the United States in recent years has been strong. The jobs market has performed well and growth has been notably higher than in other advanced economies.

And yet polling around the Presidential election found that many Americans were deeply unhappy with the state of the economy.

Of course, if voters in a relatively well-performing economy were feeling miserable then those in less well-performing ones were feeling even more miserable.

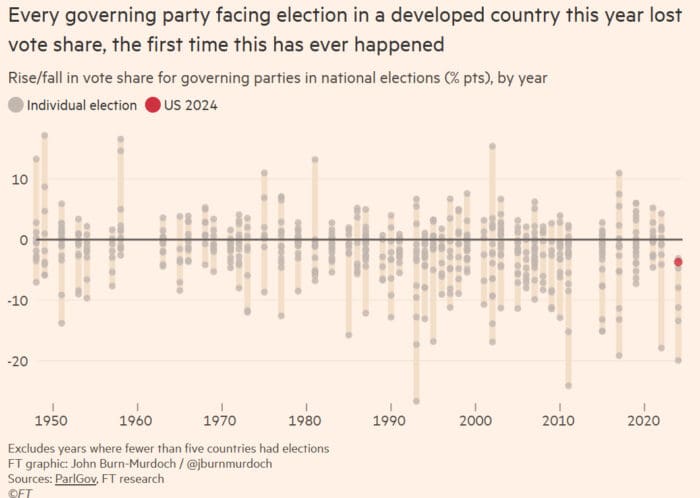

A few things leap out of this chart. Perhaps the most interesting one is that 2024 has been a worse year for incumbents facing re-election than even the aftermath of the global financial crisis was in 2008-09.

The countries where incumbents have either taken a kicking – or, like Germany expect to early next year – have in many ways varied economic performances. Britain, where the government suffered as record-breaking defeat earlier this year, has endured a recession whilst the United States experienced decent growth. What they have in common is that inflation has been at, often, multi-decade highs in recent years.

All of which has kicked off a lively debate amongst observers in recent weeks as to whether or not voters measurably dislike inflation more than they dislike unemployment.

There are plausible reasons why this might be the case. The most simple being that even relatively high unemployment rates (say 8-15%) only ever directly impact a minority of voters. It is perfectly possible for governments to preside over periods of high unemployment and win re-election as long as the wider economy is generating enough winners to maintain a voting coalition for the incumbent party. By contrast, inflation tends to produce a lot more losers as most voters see their real incomes fall.

That said, it may be that – as commentators are wont to do – too many general lessons are being taken from the experience of 2024. Some questions remain either unanswered or indeed unanswerable.

For example, if the driver of the anti-incumbent backlash in 2024 was high inflation then why did it come in 2024 – when inflation had generally fallen to more normal levels – rather than earlier during the spike of 2021-23?

Equally, to invoke a counterfactual – had fiscal and monetary been tightened aggressively sooner and had inflation been materially lower but unemployment materially higher, would voters have really thanked governments for this by re-electing them?

More specifically, even if the elections of 2024 were indeed a reflection of a global dislike of inflation over unemployment, to what extent was this unique to 2024 rather than reflective of a general rule? It could, for example, be the case that the post-pandemic price shock was felt especially acutely by voters used to three or so decades of relatively stable prices. Or that there is a tipping point at which inflation becomes so high that voters will accept higher unemployment as the cost of reducing it.

All of this matters. If the lesson politicians take from the elections of 2024 is that voters prefer price stability to almost any other benchmark for macroeconomic performance, then it is not hard to imagine them being incentivized to pursue, at times, unnecessarily tight policies in the future.

Last week the Clark Center’s European Experts Panel helpfully turned their attention to this. Their answer to the core question of whether “a period of high inflation is substantially more electorally damaging to incumbent governments in advanced countries than a period of high unemployment” was unhelpful for anyone looking for a quick take. Weighted by confidence, 30% of respondents either agreed or strongly agreed whilst just 11% disagreed. Some 58% were uncertain. In other words, more research is needed before firm conclusions are drawn.

The panel also delivered some bad news for incumbent governments everywhere. A strong majority of respondents agreed that “voters are more likely to punish incumbents for what they perceive as poor national economic performance than they are to reward incumbents for a good economy”. In other words, voters will punish economic failure, but they might not always reward economic success. It can be tough to be a policymaker.