It sometimes surprises those who do not follow fiscal policy closely just how much of the process is often based on a series of polite fictions that those involved sometimes pretend to believe.

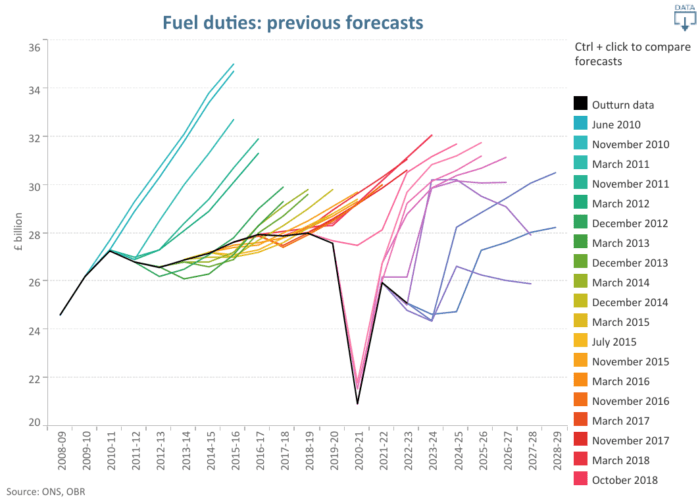

The best example comes from the United Kingdom and concerns Fuel Duty, the duty charged on motor vehicle fuels. In theory, and legally too, this duty should rise each year in line with the retail price index. At the 2011 Budget, though, the UK government not only canceled the previously announced uprating in line with inflation but also cut the duty by 1 penny. That would have been no big deal, but they then canceled the planned rise the following year and did the same again the year after that. In fact, for more than a decade now, at each subsequent budget the annual uprating has been canceled and fuel duty frozen. And each time the Office for Budget Responsibility, the independent body which monitors the government’s fiscal position and produces economic forecasts, has been forced to amend its forecasts for the coming year but dutifully go along with the notion that fuel duty will rise in the future.

The result is a very silly chart.

The black line is the actual outturn and the variously coloured lines show how the forecasts have looked at each point in time.

This fiction, the idea that Fuel Duty will rise in line with inflation over the coming years, has proved rather useful for British Chancellors since 2011. Whilst they might have never had any real intention of actually increasing fuel duty, the official budget documents banked the revenue into the forecasts making the fiscal position somewhat brighter. Over the last decade, a ‘surprise’ freezing of Fuel Duty has become as much a part of British Budget day tradition as the pictures of the Chancellor brandishing the red box for the cameras.

At least though, in the case of this particular duty, the numbers are, in macroeconomic terms, small – a few billion pounds over the coming years. That is much less the case when it comes to the Tax Cuts and Job Act (TCJA) 2017 tax changes.

The TCJA, which was passed in 2017 and came into effect in January 2018, saw substantial cuts in corporate and household taxes in the United States. But whilst the corporate taxation changes were mostly permanent, many of the household tax changes are due to expire at the end of 2025. In other words, whoever wins this year’s election will have a fairly immediate choice to make about whether to fight to extend these changes or to allow rates to revert to their 2017 levels.

In this case, by contrast with the UK’s imaginary plan to increase Fuel Duties, the numbers involved are large. Brookings put the cost of extension at $3.8 trillion over a decade.

It was these tax cuts, and the debate around them, to which the Clark Center’s US Experts Panel turned their attention this week.

The experts were first asked whether making the tax cuts due to expire in 2025 permanent would substantially increase federal deficits and the federal debt over the coming decade. The results were one of the most decisive of any poll over the past several years. Weighted by confidence, 56% of respondents agreed that extending the tax cuts would substantially increase debt levels and 40% agreed. Just 4% were uncertain about this and no respondents disagreed.

At the time the tax cuts were first proposed, the broad consensus of economists was that they would probably boost growth in the short run but that the impact – unlike the resulting higher debt – would soon fade away.

Once again, there was not much support from the experts for the notion that extending the cuts would lead to materially better economic performance over the medium to longer term. Asked whether making the reductions permanent would measurably increase US economic growth over the coming decade, 12% of the respondents (again weighted by confidence) agreed whilst 44% disagreed and 9% strongly disagreed. 36% were uncertain.

On the economics of the immediate policy question – whether to allow the temporary tax cuts to elapse – the view of the experts is clear. Extending the tax cuts would lead to materially higher Federal debt levels over the coming decade but is unlikely to have much of a positive impact on economic growth.

The final issue the experts considered was perhaps the most interesting of all, in that it cut to the heart of what might be thought of as fiscal fictions. It is often politically easier to pass a temporary tax cut than a permanent one. And given politicians face reasonably short-term electoral cycles a temporary tax cut can be absolutely ideal for them. They can have something to hand to voters in the here and now and how the budget is eventually balanced is a question for the future – and sometimes their successors.

But reversing even ‘temporary’ tax cuts can sometimes be tricky. Asked whether, given US Congressional budget scoring rules, temporary tax cuts generate sufficient pressure for extension as to be effectively permanent, the panel was divided.

33% of respondents, weighted by confidence, either agreed or strongly disagreed whilst 21% disagreed. A plurality, 46%, was uncertain.

Uncertainty when it comes to impacts and outcomes of political horse trading is understandable. Much depends on the outcomes of elections and the exact composition of Congress.

And alongside the question of whether or not to make the temporary tax cuts permanent, it should not be forgotten that there is also a third option – extending them again and kicking the ultimate decision further into the future. Fiscal fictions can last for a surprisingly long time.